The island nation of Singapore has positioned itself to be a major world financial center as the 21st century ages. Between the coming rules forcing OTC derivatives onto public clearinghouses and pushing gold and silver trading toward parity with other forex pairs by removing all taxes associated with them, Singapore will continue to see very high capital inflows from the decaying west. Now that the fear trade over a European implosion and break-up of the eurozone is subsiding it should be interesting to look at what will happen to what has been the strongest currency in Asia for the past 10 years, the Singapore Dollar.

The fear trade moved huge swaths of capital into safe-haven as well as Tier 1 capital assets during the summer. Fear gripped the banks and they needed strong assets to offset the possible default of a significant portion of their portfolios. This caused a big shift out of a number of currencies, including the Singapore Dollar.

Since Singapore's banks have significant exposure to European sovereign debt, north of 60% of Singapore's annual GDP, the potential for disaster in Europe could have been devastating on the Singapore economy. But, as the fear trade wore on the SGD kept strengthening versus the euro, this implied that the debt held was of the Northern European variety as opposed to the default-prone PIIGS variety.

Now that the major central banks have all embarked on some form of QE and the MAS (Singapore central bank) has its hands tied with both a technical recession and a potential real estate bubble the prime cause of which could be from the intense capital flight from Europe and the U.S. and not an Austrian-Economics-style bubble induced by low interest rates (though I'm sure they are helping it along). The MAS is faced with weighing a number of factors:

1. The interest rate peg to the U.S. Dollar can now be loosened slightly because banks like DBS Group can better weather the current slowdown in real estate now that their exposure to Europe has been back-stopped by the E.C.B.

a. This would attract more investment capital and promote savings, needed to build GDP growth.

2. While the SGD has risen slightly (5% in the past 2 years) versus the Malaysian ringgit, Malaysia being its strongest trading partner, it will rise quickly versus both the yuan and the Hong Kong dollar because of their pegs to the U.S. dollar. The MYRSGD has been stable all summer at 0.400.

3. By allowing the exchange rate overall to increase steadily it will promote gold and silver storage locally, which is part of its plan in building a number of vaults around the island to house precious metals as well as removing all sales taxes on gold and silver bullion trading.

With the EURSGD trading near the important S$1.58 level right now it will be interesting to note if the MAS continues play against the mercantilist competitive devaluations going on around the world, gladly scooping up real assets at increasingly cheaper prices. The short-covering rally in the euro seems to have taken a pause as the markets wait for E.C.B. President Mario Draghi to actually fire the howitzer he has in his hands (OMT, ESF, etc.). Spain or Italy will have to ask for a bailout and are holding out looking for a better conditionality deal. It is my bet that any package tied to a bailout will involve the sovereign gold of the countries involved and that's where the hold up lies. Between now and then expect the headlines to manage the price of these currencies on a day-to-day basis, while the fundamentals continue to build until a compromise is found.

When that happens, the euro will explode versus the U.S. dollar to the upside and the CurrencyShares Euro ETF (AMEX:FXE) will move quickly. I like selling $122 January 2013 puts into this euro rally right now as there is very little risk of the euro moving back below $1.22 at this point. If early in October the euro breaks above the Sept. 17 high of $1.3172, I would take 1/3 of the money from the premiums from selling puts and buy January calls above $135, effectively doubling down.

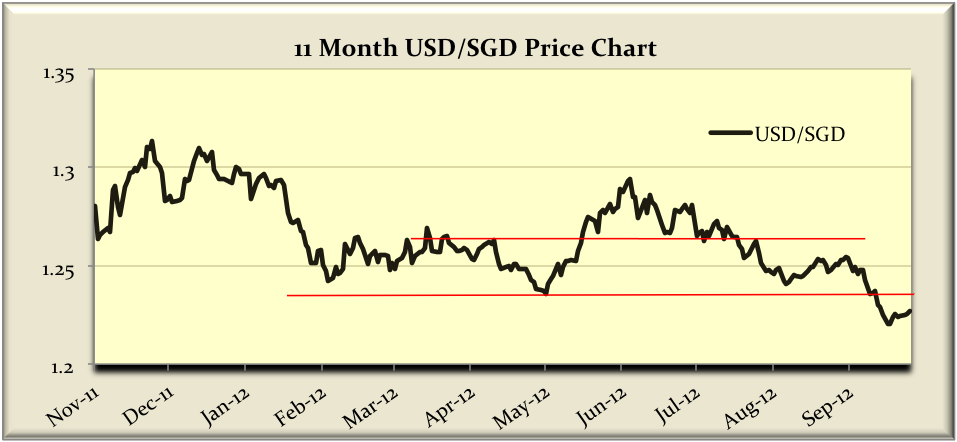

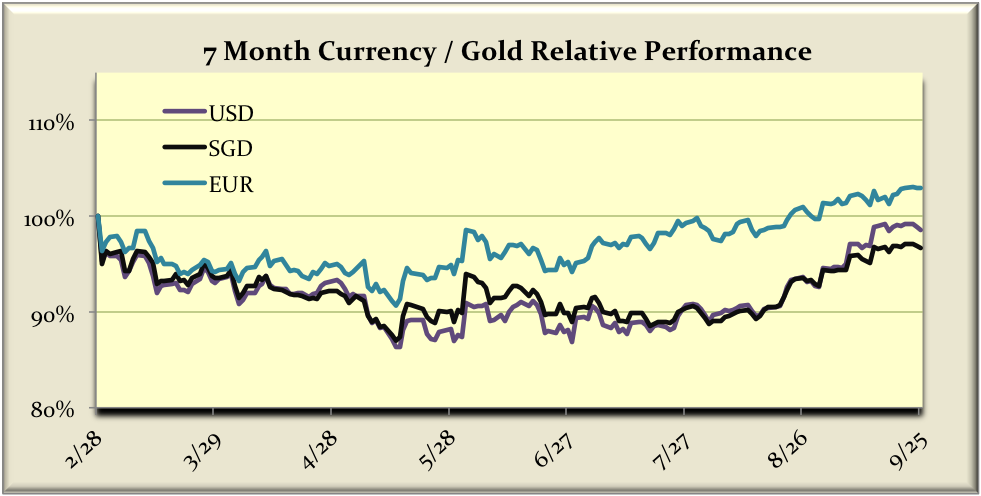

The Singapore Dollar will suffer in the short-term but overall the 10-year trend of the EURSGD is down and intact.The USDSGD trend is similar and also completely intact. If anything the relationship is even more in Singapore's favor with the USDSGD having broken below the April 30, low of S$1.2348. Even with this pause in the euro there has been little appreciation of the dollar versus the SingDollar. The all-time low is near $1.20 and that should be tested before the end of the year.Once the new gold and silver trading rules go into effect Singapore will see more trading in its local markets and gold will flow into the country. This is especially true if the MAS resists debasing the SingDollar.I am not as big a fan of the SPDR Gold Trust ETF (AMEX:GLD) as I am the Sprott Physical Gold Trust (AMEX:PHYS). Physical gold being removed from the market, which cannot be reallocated and rehypothecated is itself bullish for the gold price by restricting supply. Note that since the QE announcement the SingDollar has outperformed both the dollar and the euro with respect to gold. I would expect this to become a self-reinforcing relationship

The quarterly close tells us a number of things. A number of markets were pulled back to the middle of their monthly ranges to put doubt as to what direction they would move in October. The EURUSD closed at $1.2848, which was a completely neutral price but the uptrend is still firmly in place and the rally should continue through year end with a real possibility of $1.40. The USDSGD closed at S$1.2275 and the EURSGD at S$1.5784 below key support (see chart above), which means that no matter what EURUSD does day to day the trend there is also firmly intact.These markets have their fundamentals in place and from a short-term perspective; rallies in the USDSGD and EURSGD pairs and pullbacks in gold should be bought. As a supporting signal of the USD's weakness the USDCNY pair hit an all-time low on Friday's close as well; this indicates that the Fed has gotten what it wanted, a slowing of the capital flow from the U.S. to China via the appreciating Yuan.

0 comments:

Post a Comment