Fundamental Forecast for New Zealand Dollar: Neutral

- Dollar Vulnerable on US Data Surprise Risk, EU Summit Fails to Excite

- Investors Drop Safe Havens in Favor of Aussie, Euro Amid Bailout Speculation

- New Zealand Dollar Subject to Risk Trends

The New Zealand Dollar had a mediocre week, finishing in the middle of the pack among the majors and dropping by a mere -0.10% against the US Dollar. Needless to say, if the NZDUSD was essentially unchanged on the week, risk sentiment could not have been all that bad. Of course, the Kiwi was weaker headed into the last part of the week, as high beta currencies and risk-correlated assets topped out on Thursday after a decent third quarter Chinese GDP print, and then the Euro-zone Summit disappointed by its culmination on Friday.

These setbacks leave anything with a yield in a precarious situation, as investor confidence is increasingly feeble for a number of reasons. First, the Euro-zone Summit offered little progress on anything material in the near-term. The hope was, at least from this analyst, that some of the chatter we’ve heard over the past few weeks was an indication of something bigger and different in the works. But, as the saying in technical analysis goes, “the trend is your friend,” and thus we should expect future Euro-zone Summits to be nothing short of failures until they’re not.

Developments in the Euro-zone crisis are crucial to New Zealand Dollar. As noted on numerous occasions in the New Zealand Dollar Weekly Trading Forecast, “On February 6, Moody’s Investors Service said that the New Zealand economy was among the “most exposed” to the crisis, further noting that its banking system (along with Australia’s and Korea’s) is “more vulnerable to the first-round impact of a further worsening of the euro area crisis than other systems in Asia Pacific.” Now that Euro-zone issues are coming back – we’ve seen leaders’ attempts to stabilize markets fail in October and November 2011, late-February and early-March 2012, and then again after the Spanish bailout in June 2012 – the New Zealand Dollar will be most exposed. The question is: will the European Central Bank’s September efforts join this list of doomed promises?

The second influence, the Chinese growth story, is looking kinder. In fact, data has started to trend higher and inflation looks well-contained now that growth is slowing and the Chinese Yuan is gaining value against the US Dollar. Taking a look at recent moves from the People’s Bank of China, it is not a far reach to suggest that policymakers are using the Yuan’s exchange rate as a policy tool: if inflation cools too much, they can allow the Yuan to depreciate, for example.

The last influence on risk trends, to which the Kiwi is very much tied to (as established above), did not come into play in a major fashion, but it is certainly getting close to there. The US fiscal cliff prompted the first of the big banks, JPMorgan Chase, to cut its 2013 growth forecast to +1.0%. Anxiety is building as the US Presidential election cycle comes to a head, and with the candidates meeting daily with media and weekly for debates, a lot of focus is being drawn to the American fiscal mess. As we saw in the summer of 2011, US fiscal concerns are supremely negative for the New Zealand Dollar.

While these exogenous influences will both boost and weigh on the Kiwi, there are also some important domestic events on the docket this week that will guide price action.

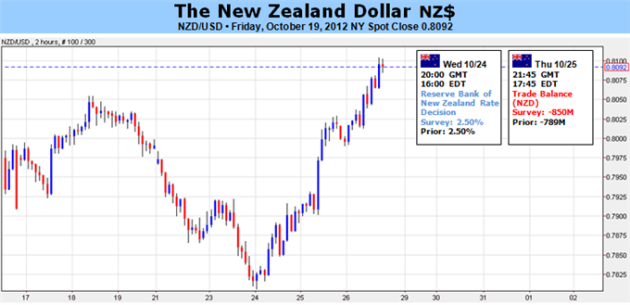

On Wednesday, the most important event of the week, the Reserve Bank of New Zealand Rate Decision, takes place. The RBNZ is expected to leave the key interest rate on hold at 2.50%, where it has been since March 2011. Negative rate expectations have been building into the Kiwi, and there are now -26.0-basis points being priced out over the next 12-months, from +1.0-bps being priced in on September 18. If the RBNZ draws attention to the three aforementioned points, we suspect there could be some more downside left in the New Zealand Dollar (we saw the Reserve Bank of Australia issue some concerns over global growth, Asia, and Europe a few weeks ago in their October meeting, and that weighed on the Australian Dollar; they also cut rates).

With nothing major expected from the RBNZ, there’s also the September Trade Balance due on Thursday. The stronger New Zealand Dollar last month (rebounding from mid-summer lows) is expected to have boosted the deficit, from –N$789M to –N$850M. The Export figure is of greater interest than the Import figure, given the concerns over slowing growth in Asia; that will be the key metric to watch. If better than anticipated, the trade report could keep the Kiwi elevated into the end of the week.

Overall, global risk trends and domestic New Zealand data and events aren’t enough to offer a clear picture for the week ahead, and we thus are choosing to take a “neutral” bias once more. Accordingly, we note that the firming in Chinese data offers the clearest picture for the Kiwi in context of the renewed concerns out of Europe, which means that if risk-aversion is rampant, the European currencies are likely to depreciate more than the Asian-Oceanic currencies. As long as the NZDUSD holds 0.8110 next week, the potential remains for a run back to 0.8300.

0 comments:

Post a Comment