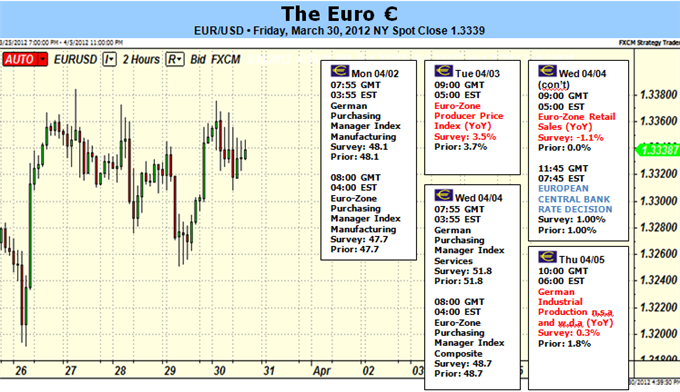

Euro at Crossroads, ECB and US Nonfarm Payrolls May Set Pace for Q2

Fundamental Forecast for the Euro: Neutral

- Euro gains asEU officials boost bailout capacity – further room to run?

- European March Consumer Confidence weak, dampens enthusiasm

- EURUSD challenging key resistance near $1.34, next move critical

The Euro ended the month of March unchanged against the US Dollar (ticker: USDOLLAR),

but an otherwise strong first quarter sets the pace for further EURUSD

gains in 2012. Yet the coming week of major event risk may prove

critical for the Euro and US Dollar as the exchange rate trades near

significant technical resistance and at a major crossroads.

All eyes turn to European Central Bank for a

highly-anticipated rate decision due April 4, while a potentially

game-changing US Nonfarm Payrolls will wrap up what could be a pivotal

week in price action. European officials took some pressure off of the

Euro as they agreed to boost the firepower of their key bailout funds.

Yet it will be important to watch whether ECB President Mario Draghi

hints at further monetary policy support for the at-risk Euro Zone

economy.

Recent Euro Zone Consumer Price Index data showed

year-over-year inflation dip to its lowest levels since August, which

may give the ECB the reason it needs to ease policy further. The yearly

rate of 2.6 percent remains above official ECB targets of 2.0 percent;

yet the trend favors further slowdowns outside of volatile energy

prices. Is it enough to warrant further easing? Only the ECB itself can

make that decision, and all eyes remain on Draghi’s rhetoric.

Across the Atlantic, the US economic calendar brings

its usual slew of early-month data and of course the infamous Nonfarm

Payrolls result due Friday. NFP’s are almost always market moving, but

March numbers carry extra weight due to recent shifts in rhetoric from

US Federal Reserve Chairman Ben Bernanke. Bernanke rekindled speculation

that the Fed would enact another wave of Quantitative Easing (QE3) when he warned that the economic recovery seems fragile and the Fed stands ready to increase stimulus if the need arises.

The Chairman specifically cited a sluggish labor

market as a risk, but the past several months of US Nonfarm Payrolls

data have seen domestic unemployment rates tumble from 9.1 percent in

August to 8.3 percent in February.

Ongoing improvements in the US labor market have

almost certainly contributed to the best single quarter of Dow Jones

Industrial Average gains since Q1, 1998. Is such optimism sustainable?

If history is a guide, the Dow move mostly sideways in the quarter that

followed those major gains in 1998. It only traded to further highs

through the end of the year. And past performance is not indicative of

future results, but an 8.1 percent Dow rally in the first three months

of 2012 translates to a massive 38.7 percent annualized return. Only

1954 and 1975 produced such lofty annual returns in the Dow dating back

to WWII period. One can never say “never”, but a repeat seems unlikely

given significant macroeconomic risks across the globe.

If we do see a significant correction in the US

Nonfarm Payrolls and similar pullbacks in the Dow, we might expect the

safe-haven US Dollar to outperform the Euro and other key currencies

(EURUSD decline). Indeed, the Dollar-Dow correlation trades near record strength as US interest rates are near record-lows.

Needless to say, any major surprises in key data and

events in the week ahead could be the catalyst to force big moves. We

remain in “wait and see” mode as the Euro trades near critical

resistance and Q2 promises big moves across financial markets. – DR

0 comments:

Post a Comment